Well, it’s just about a decade since the Great Recession began and I suppose it is natural to look back and reflect on both the pain and the promises of that tumultuous time in US history. Fueled by very irresponsible lending/borrowing behavior, the economic downturn is traced by the National Bureau of Economic research (the entity who is, according to the Wikipedia article, the official arbiter of US recessions) to state that it began in late 2007 and extended deeply into 2009, leading to 19 months of negative growth.

Widely regarded as the worst global economic crisis since the Great Depression, the Great Recession has elicited quite different responses depending on the responder's point of view.

For some, the depth of the Great Recession was mild in comparison to the Great Depression. Peak unemployment rates during the latter reached 25% compared to 10% sometime around October of 2009 (according to the Bureau of Labor Statistics or BLS). Misery and poverty were commonplace in the Great Depression on a scale that far outweighed anything seen before or since.

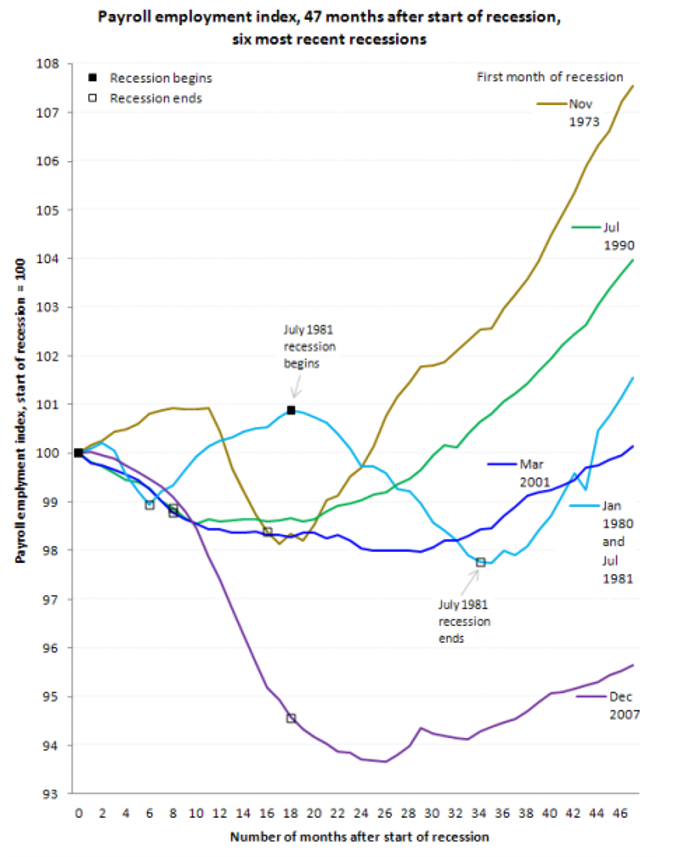

For others, the Great Recession brought real and lasting pain in the here and now; pain all the more exacerbated by the fact that the Great Depression ushered in a whole spate of policy techniques designed to help political leaders and economists avoid these sorts of downturns and to blunt their effects. In particular, payroll employment dropped far more sharply than in the previous 5 recessions and persisted in this weakened state.

The previous graphic was taken from The Recession of 2007-2009, a fascinating (and sobering) summary of the Great Recession by the BLS that drives home just how devastating that period in US history was.

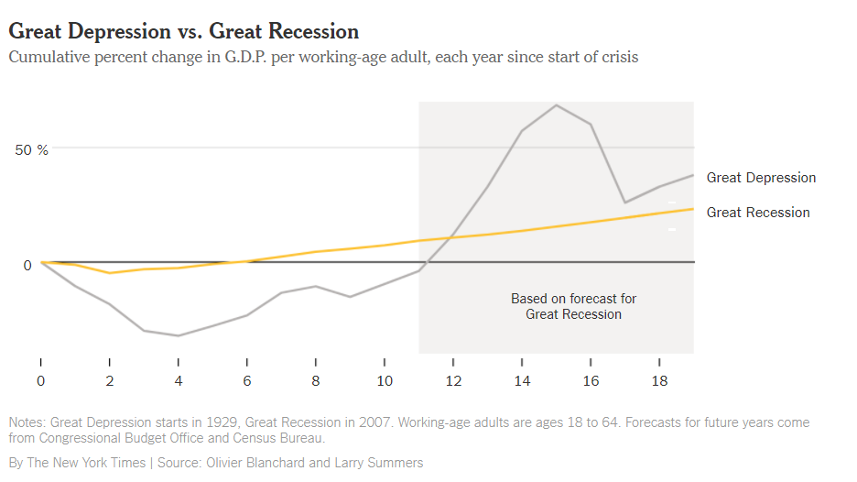

Nonetheless, the general impression is that, as a whole, the US is better off now than it had been in the aftermath of the Great Depression. But, as pointed out in the article We’re About to Fall Behind the Great Depression by David Leonhardt, the recovery from the Great Recession has languished in comparison to its much-worse predecessor.

Leonhardt based he’s claim on a graphic produced by Olivier Blanchard and Larry Summers that shows the GDP per capita for adults aged 18 to 64 scaled by the number of years since the onset of the economic crisis.

Blanchard and Summers base their onset of the Great Depression with the Stock Market Crash of 1929 but there is some dispute over whether this event caused the Great Depression or whether subsequent policies turn a market correction into a full-blown catastrophe. Nonetheless, the initial dip in GDP per capita from this starting point was a great deal more pronounced (gray line) than the dip after the onset of the Great Recession (gold line). And the loss of relative wealth was also more severe in the Great Depression (year 4) than in its smaller counterpart. But the overall recovery was more pronounced by the twelfth year than the recovery of their prediction of where the trajectory of post-2009 US is headed.

Blanchard’s and Summers’s chartsmenship (or at least the NYT’s reproduction) leaves a lot to be desired and surely they’ve engineered the presentation of the data to obscure the fact that the US involvement in World War II began at the twelve-year mark. Nonetheless, I believe their basic message is correct. The US recovery since the end of the Great Recession has been anemic at best.

There are a host of reasons but they all fall under one broad umbrella – government policy and regulation during the aftermath of the Great Recession.

As is widely discussed, the US has one of the highest corporate tax rates in the world. In addition, the US taxes companies who earn a profit overseas; they are taxed by the country in which they earn their profit and then are taxed a second time by the US if the company tries to bring that profit back into the US. This has caused many companies to keep their profit invested in the countries in which they earned it and out of the investment markets here at home.

In addition, the regulatory structure has increased to unbelievably burdensome levels. As discussed in a previous post (Haircuts and Wine), the single biggest obstacle to small business creation and subsequent innovation is the compliance burden visited on these entrepreneurs. Since the bulk of small business profit and investment is done here in the US, regulatory hurdles and higher tax rates offer a double-whammy to increasing economic growth.

Another insidious and perverse aspect of federal policy is the growth of government largesse and the increasing incentives for people to get on the public dole and hang out. Having a larger percentage of the population taking rather than giving hurts not only their dignity but the morale of those producing that which the takers are consuming. Thus there is a two-fold hit to productivity – the loss of all the capability of those standing on the sidelines and the loss of motivation by those still in the game.

So, even though I think Blanchard and Summers slanted the presentation a bit with their graphic, if it serves as a rallying point for improving the economy then so much the better.