In his book How to Lie with Statistics, Daryl Huff points out that misleading statistics are used so often by members of the fourth estate that it is difficult to truly believe that it is due to happenstance and a poor understanding. It seems more likely that the use of misleading statistics to sensationalize is deliberate, although proving it so is impossible. In this way, there is overlap between his observations with that old maxim

So too goes for the law of unintended consequences, where a new maxim of economics might be read as

What brings this grim pronouncement to this month’s column? Once again, the Wise of Sacramento have created a set of incentives that they claim will help the average California resident, but which are subverting the insurance market in the golden state. Large insurers are either scaling back (Chubb and AIG) or are refusing to issue new homeowner policies altogether, as is the case with State Farm and Allstate, California’s 1st and 4th largest insurers of residential property.

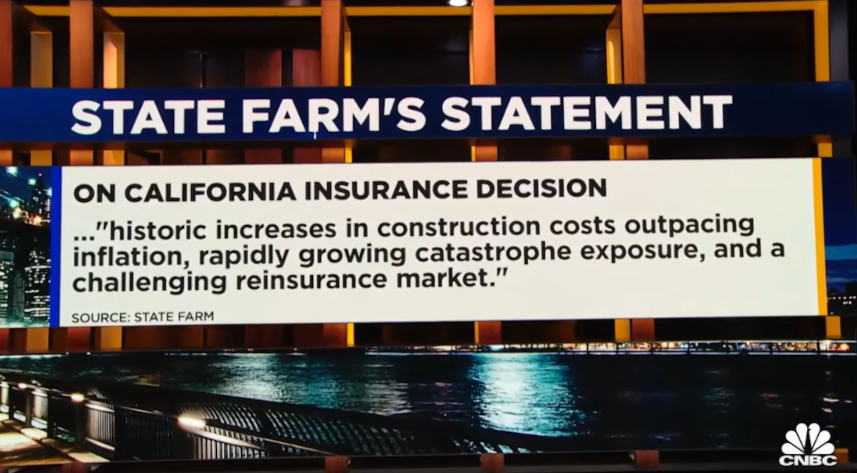

To be fair, in their press announcement, State Farm cited three reasons for their discontinuance of new policies: 1) increasing wildfire risk, 2) rising home construction prices that outstrip inflation, and 3) a challenging reinsurance market.

Can all of these woes be laid at the feet of governance? Well, while California’s state legislature is not entirely responsible for the first two items, they are certainly not blameless.

In his article Of Course Home Insurers Are Fleeing California, Mark Gongloff, of Bloomberg, points out that California ‘NIMBYism’ has driven non-affluent residents to build in higher risk areas. Once these homeowners are established in this high-risk zones, the state does little to protect them from wildfires as the CNBC’s host of the discussion and analysis in the video Insurance is the effect not the cause, says III CEO Kevelighan on State Farm’s California decision points out:

Regarding the construction costs Gongloff points out that

This, in effect, favors higher-end construction costs state-wide, an outcome that Sacramento seems quite content to ignore.

But the most damning indictment against California governance is its insane regulatory structure. While the state legislature does little to curb estate development costs it seems quite comfortable in exercising its regulatory muscle to force insurance companies to keep costs artificially low.

In her article Why insurance companies are pulling out of California and Florida, and how to fix some of the underlying problems, Melanie Gall, Co-Director of the Center for Emergency Management and Homeland Security, Arizona State University, poses the question

The obvious answer to this is California’s proposition 103 that limits premium increases to homeowners, prohibit policy cancellations and require certain levels of coverage, all of which effectively eliminate ways in which the insurers can mitigate risk from the consumer side.

According to Gall, the chief executive of the insurance company Chubb’s

Steve Forbes, in his video California’s Insurance Catastrophe Explained—How Government Caused Another Crisis | What’s Ahead, puts the matter much more forcefully, blaming the regulatory structure imposed on the states insurers as keeping premiums artificially low.

This sentiment is shared by Gongloff, who writes that

Insurance Information Institute CEO, Sean Kevelighan, in a clip from the CNBC video cited above, lists the numerous issues that Proposition 103 turns a blind eye to.

The damage caused by California’s heavy-handed regulatory structure doesn’t end there. As Gall points out,

The consequences (unintended or otherwise) of such perverse incentives is that insurance companies know full well the actuarial risk they are being forced to take but can do little to share that risk with the home owner. As a result, they are also impeded in getting reinsurance, which Investopia defines as insurance for insurers, which transfers risk to another company to reduce the likelihood of large payouts for a claim, thereby allowing insurers to remain solvent by recovering all or part of a payout.

Gall cites the rising costs of reinsurance by noting that

And, so, we find that rather than expose themselves to additional risk that could conceivable bankrupt the company, insurers are simply opting out. The consequences of this move are far-reaching. This leaves California as the insurer of last resort through their FAIR plan, which provides basic fire insurance coverage for properties that can’t secure policies through traditional means.

Once again, Steve Forbes pulls no punches in his assessment of the scope and financial soundness of the FAIR plan.

Of course, one might think that Sacramento would change course when confronted with all of this overwhelming evidence of how California’s regulatory structure is causing more harm than good. But, one would be wrong. The prevailing sentiment seems to be one in which ‘greedy’ businesses are blamed for not being good corporate citizens and must be forced businesses into doing things against their financial well-being, as Gongloff notes:

Sadly, this debacle is only one battle in an ongoing, subversive war which California governance seems to be waging against common sense and the citizens of a once great state. Enemy action indeed.