US Debt History

Here we are at the end of September and the threat of a government shutdown, which is very likely to be realized in a few days, dominates much of the news landscape. Of course, most aspects of American politics are deeply polarized but the subject of a shutdown seems to ratchet up the rhetoric even higher. The are many aspects of contention between the various factions but one item lies firmly in the economic sphere, namely government debt.

The first debt the country would end up carrying was a result of the expenses incurred in fighting the Revolutionary War to its successful conclusion in 1783. After the establishment of the Constitution in 1787, this debt became a point of contention between the Northern States, which most held it, and the Southern States, who did not want to assume it as a joint debt of the combined union. The Compromise of 1790 resolved brought the two sides together with the South agreeing to make the debt held at the federal level and North, who conceded the permanent location of the national Capitol in Washington D.C., located on the border between Maryland and Virginia.

During the ensuing 232 years, the debt has fluctuated up and down in response to various exigencies experienced by the country. Since inflation lowers the purchasing power of a fixed amount of money the usual way to track the debt is as a percentage of gross domestic product. This will be the sole measure used in this discussion.

Historical data for the time span of 1790 to 2000 is available from the Congressional Budget Office (CBO). Those data were combined with data from 2000-2022 available from the St Louis office of the Federal Reserve.

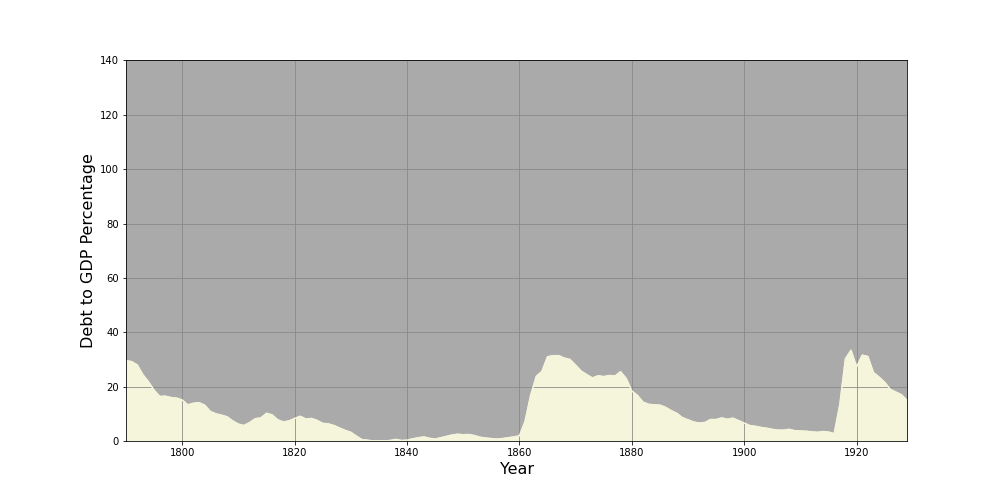

Over the time span from 1790 (debt inception) to 1929 (year of the bank panic), the percent of debt to GDP never went above 40% and the three increases are all associated with a major war: the first peak from the original debt from the Revolutionary, the second due to the Civil War, and the third in and around World War I. The average debt held during this period of time was approximately 11.2%.

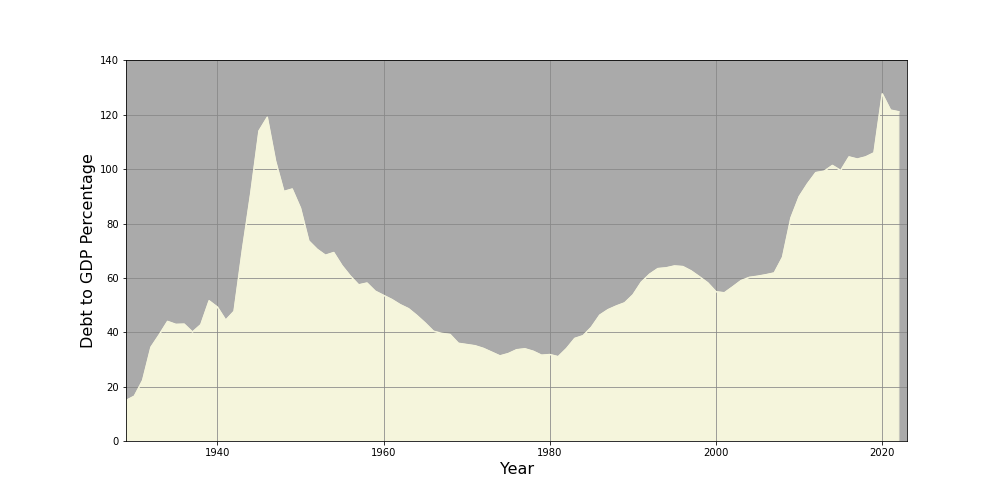

Over the time span from 1929 to 2022 (the last full year with reportable statistics), the ratio of debt to GDP only went below 40% on two occasions. The first is in the period of time from the bank panic in 1929 to the most serious part of the Great Depression in 1933. The second is from 1967 to 1984 during the tumultuous economic times of the 1970s. From 1992 to 2007, the ratio hovered around 60% but then shot up rapidly after the Great Recession, most likely due to the increased government spending associated with quantitative easing that was employed during that time period as means of addressing the aftermath of the housing market catastrophe. The level increased again to its current level during the time of the pandemic. The average debt held during this time period was approximately 60.8%.

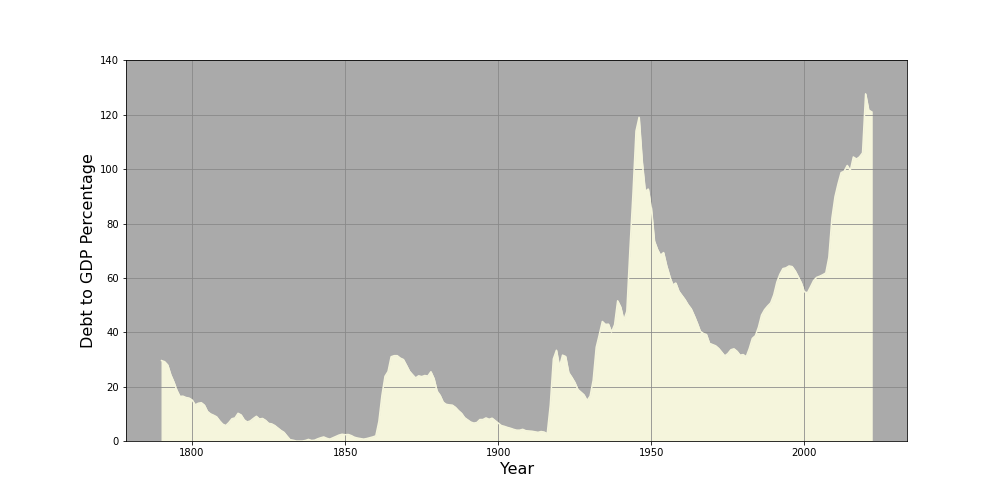

Obviously, there was a fundamental shift in governmental fiscal policy in the 139 years prior to the Great Depression when compared with the 92 years following. This fundamental shift is most easily seen in a plot of the entire time range.

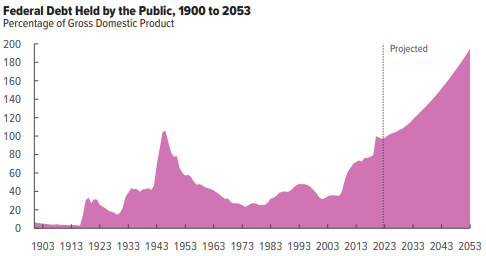

Debt to GDP has never been as high as it is now, not even during World War II, when the country faced an existential threat.

Debt to GDP has never been as high as it is now, not even during World War II, when the country faced an existential threat.

So, the key question is: are we getting our money’s worth from all this spending? Proponents point to the amazing standard of living we enjoy – in particular, to the various entitlement programs aimed at protecting the most vulnerable amongst us and to the highly technological and productive work force we employ who generate the material wealth even the poorest of us commands. Opponents point to the numerous examples of waste and fraud, the inefficiencies, and, ultimately, to what they perceive as the unsustainable trajectory US debt is on. The following plot from the CBO underscores their concerns.

Unraveling these arguments to find the truth is difficult because arguments on both sides often involve hypotheses contrary to fact fallacies. Perhaps with a more laisse-faire approach to the economy we would be enjoying a greater standard of living than what we have now with a far smaller fraction of people below the poverty line. Perhaps more spending is exactly what is needed to jump-start growth and lower poverty.

That said, I find the arguments made by men like Thomas Sowell and Milton Friedman compelling. These economists base their arguments on careful time-based and lateral studies that, while not completely free of counterfactual reasoning, come as close as any social scientist can to objective studies of the economy that parallel how physical scientists study nature. They argue quite persuasively that the ratio of debt to GDP is too high to bring benefit to the average citizen. Sadly, neither their arguments nor, for that matter, the arguments of economists supporting the opposite viewpoint are presented in a comprehensive way to the public.

Where exactly will the debt debate land? At the time of this writing, it isn’t clear at all what will happen next, but whatever does it is likely to involve more sound bites than sound arguments.