Rampant Economic Ignorance

Most everyone knows what the term ‘illiteracy’ means, even those who can’t read and the shame of illiteracy is so great that people often go to great lengths to hide the fact that they can’t read – a feat best pulled off by the functionally illiterate (consider the made-for-TV movie Bluffing It starring Dennis Weaver). The city of Baltimore even went to great lengths in the late 1980s and into the 1990s to declare itself ‘the city that reads’ since alarmingly large number of the citizens were functionally illiterate.

A smaller class of people feel shame at being illogical. In certain quarters, a lack of self-reflection and internal consistency in how one argues is often excused by appealing to feelings. “I’m passionate about it” or “it doesn’t feel right” are common enough excuses used to exempt the arguer from the burden of rationality and accountability.

By the time we get to innumeracy, the shame has all but vanished, all pretense to having to excuse oneself for a lack of a vital societal skill has dropped away, and in its place is a particular pride in this particular brand of ignorance. The inability to deal with mathematics and, especially, large numbers is seen as a badge of honor.

But the proverbial three monkeys of ‘see’, ‘hear’, and ‘speak’ no evil have nothing on the alarming mix of the above three styles of ignorance to form the alarming way in which modern citizens consumes matters economic. For the purposes of this article, I’ll call this tripart, lethal cocktail of ignorance rampant economic ignorance (REI).

Case in point, the widespread claims that the oil companies are price-gouging.

To be clear, I am not definitively claiming that the oil companies are not price-gouging but I strongly doubt it for the simple reason that I can’t then explain what they were doing when prices were low. What I am claiming, with dispositive evidence, is that the average person who holds that position is indulging in merry mix of innumeracy and illogical thinking with a dash of functional illiteracy thrown in to spice things up. In what follows, I’ll go through some of the evidence offered (there is simply too much to be comprehensive) and point-out those items that caught my eye.

Let’s start with the REI on display in Politifact’s article entitled (as far as one can tell) Yes, oil companies are reporting record breaking profits. But it follows pandemic-fueled losses. In this article, author Andy Nguyen attempts to ‘fact-check’ a Facebook post that reads

To start, Nguyen only mentions in passing that Dan Price was the CEO of a company “that made headlines in 2015 when it raised minimum salaries for employees to $70,000” but doesn’t discuss that Price is likely a less-than-honest authority on any aspect of the economy base on the many criticisms heap on this ‘headline event’ of 2015 (see The Gravity of a Minimum Wage for a summary).

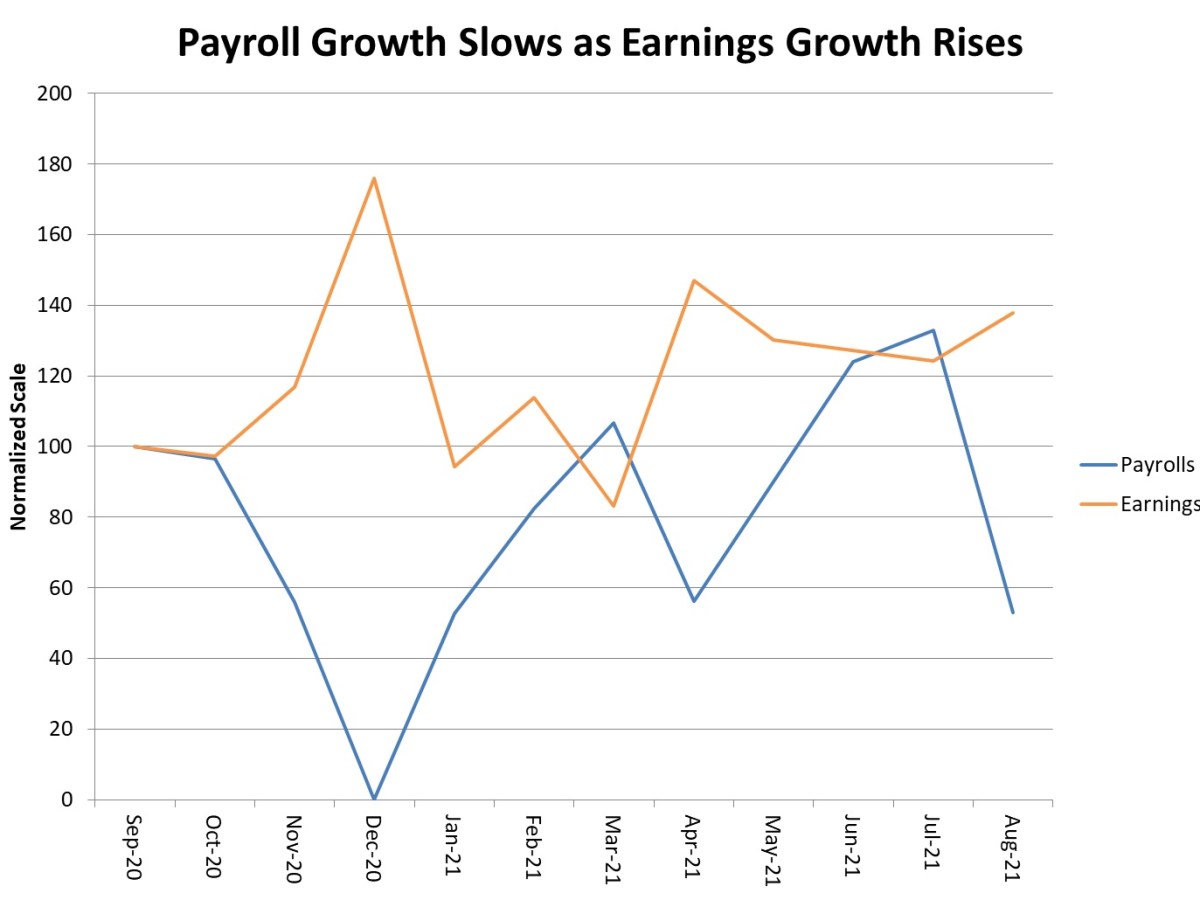

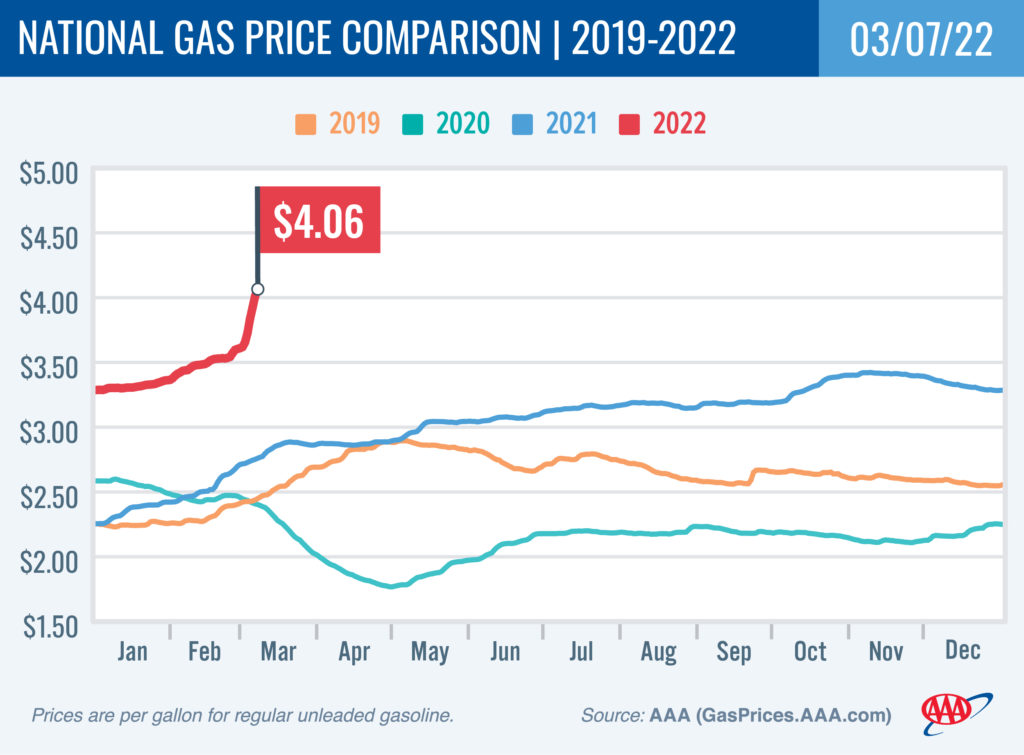

Nguyen this proceeds to provide a serviceable but somewhat disjointed context in which to place the rise in gas prices. Somewhat annoyingly, he fails to provide the following graph

the original of which can be found here. While this graph is far from perfect, it does demonstrate that gas prices were rising significantly over calendar year 2021 (year-to-year increase from approximately $2.25/gallon to $3.35/gallon) at an average increase of about 9.2 cents/gallon/month compared with the 35.5 cents/gallon/month increase in 2022. The lack of analysis here speaks of innumeracy.

Next Nguyen fact checks Prices assertion that the US only receives 1% of its oil from Russia and finds that assertion wanting in that the number is a factor of 3 lower than the truth. To this correction I say so what. Without proper context it is impossible to tell whether a 1% or 3% (whichever it may actually be) drop in quantity supplied is significant. What is needed is the elasticity of the crude oil market – a fact seemingly ignored. Chalk one up for illogical discourse.

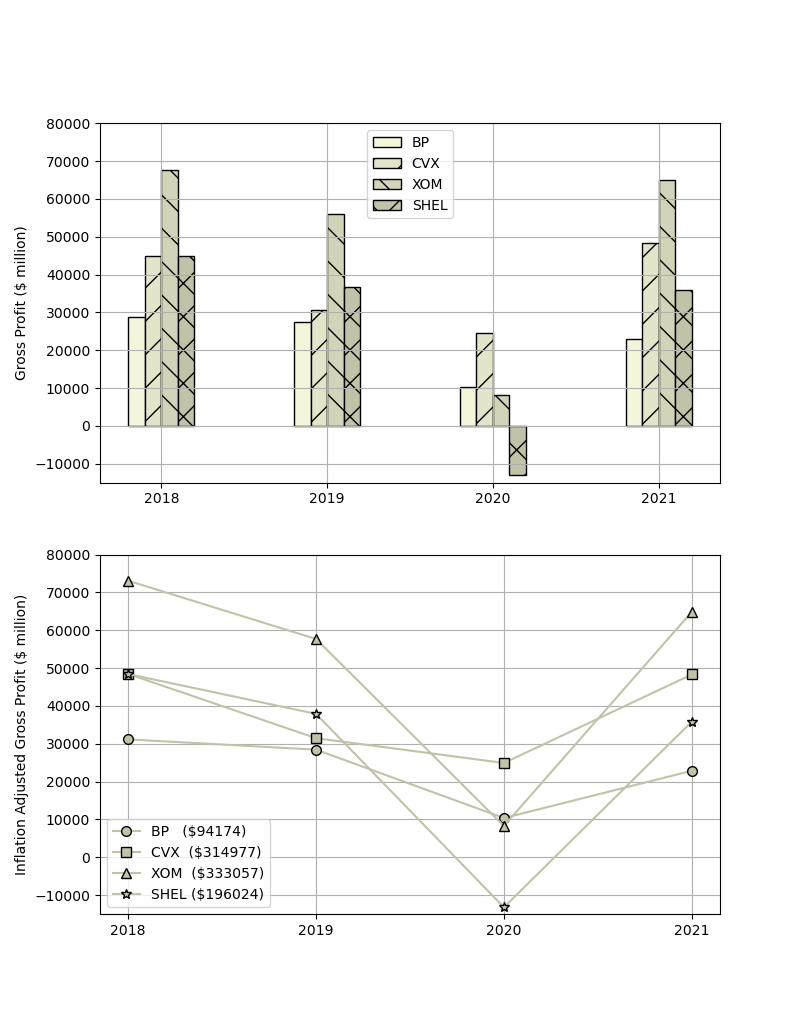

Finally, we get to an analysis record profits for the oil companies. However, there is no way to make an apples-to-apples comparison. Consider the constantly shifting ways in which the ‘profitiability’ of the big four oil companies of BP, Chevron, Exxon, and Shell are described:

- Exxon Mobil made $23 billion in profit for 2021

- Chevron… reporting in January that it made $15.6 billion in revenue for 2021…

- BP reported it made $12.85 billion in 2021…

- Shell made significant profits in 2021, earning $19.29 billion for the year…

Anyone who has ever bothered to take the time to read a company financial disclosure form would know that ‘revenue’ is a well-defined term that may, or may not, mean the same as the vague term ‘earnings’ and that neither is ‘profit’ and that there are many possible meanings for ‘profit’. And let’s not even speak about how the word ‘made’ is totally ambiguous. Score several for illiteracy.

Since most people are complaining about profit, I looked at two possible definitions: 1) gross profit and 2) net income common stockholder. I tabulated these data for calendar years 2018-2021 (the years in which the money was earned and not in the years reported) from Yahoo Finance (e.g., Exxon data), cross-checked with SEC filings available in TD Ameritrade and present both raw data and inflation-adjusted data using the schedule of 1.8%, 3.1%, and 7.9% to express 2020, 2019, and 2018 dollars in 2021 terms based on estimates found here.

For gross profit we have

where company is identified by its ticker symbol (BP = BP, CVX = Chevron, XOM = Exxon, SHEL = Shell). The numbers in the parentheses represent the market capitalization in millions as of 3/18. Only Chevron showed an increase in gross profits and the amount is extraordinarily hard to see.

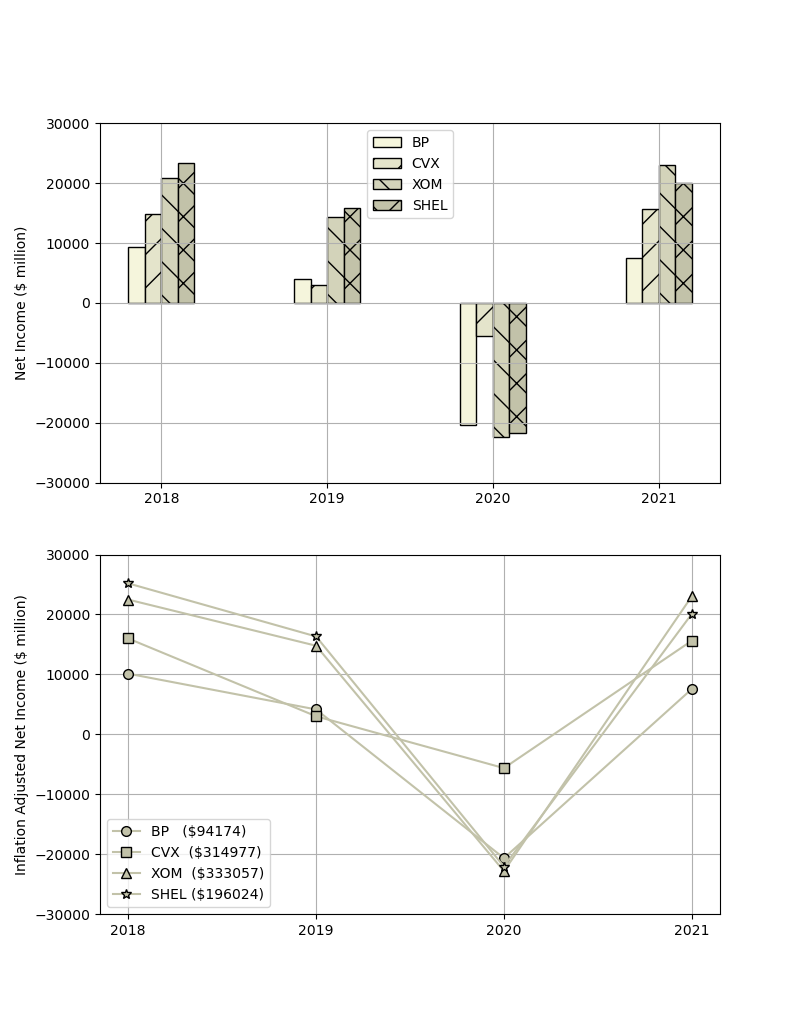

Likewise, the plot for net income common stockholder (expressed simply as net income)

shows little in the way of obscene profit-taking. Only Exxon posted a marked, but still small, increase in this definition of profits.

Where is the pricing gouging in these plots? Beats me. Neither of them show little in the way of ‘soaring’ or ‘vastly improved’ numbers spewed forth by the media.

So, how did the oil company execs and consumer advocates come to both agree on the ‘underlying truth’ of record profits (although each group interprets what that assertion actually means)? I think there is ‘Bootleggers and Baptists’ phenomenon going on here. Oil execs want to talk profits up so that investors will invest in ‘a bright, industrious company with a shiny future’. Media pundits and consumer watchdogs want to talk profits up so that the narrative of evil, price-gouging corporations will prompt governmental action. However, as the data clearly, show, if there are huge profits being made then they are well-hidden indeed.

As a final thought, one may ask oneself how can we all learn to think through these issues better? The only way I can see if for all of us to prioritize stamping out REI. Maybe with a campaign, perhaps with a slogan like “Thinking economics is fundamental”.